In the shadowy world of white-collar crime, a simple yet powerful concept of psychological behavior behind fraudulent activities emerged. Fraud triangle theory was first proposed by criminologist Donald Cressey in 1953. Now it has become the center for risk assessment and prevention strategist processes worldwide.

According to the Association of Certified Fraud Examiners’ 2022 Report to the Nations, organizations lose an estimated 5% of their revenue to fraud each year

According to a report of 2022 by the Association of Certified Fraud Examiners (ACFE), organizations face an estimated loss of 5% of revenue every year due to fraud. According to this fraud rate, the global fraud loss is approximately $4.7 trillion annually.

The fraud triangle is a framework based on why people cross boundaries to commit financial crimes. Examining the different factors wasn’t an effective conclusion instead of taking preventive measures.

The fraud model suggests three key elements for fraud to occur

- Pressure

- Opportunity

- Realization

Read on to learn more about each factor of the fraud triangle, the fraud triangle theory, How they contribute to fraud, and how you can prevent them from occurring.

1- What Is The Fraud Triangle?

The fraud triangle is the representation of the factors or elements that come to a person’s decision to commit fraud in a workspace. This was developed by Dr. Donald Cressey.

The model is based on the research of people caught in embezzlement.Most of the individuals who commit financial fraud or occupational fraud are not criminals.

When an employee commits fraud they get a chance not to be caught. They come up with a justification for their unexceptional behavioral act, that falls into committing an occupational crime.

Most of the time it’s their first criminal act. But what factors make them to do so we will explore this with the fraud triangle’s three factors theory.

What Is Fraud?

The fraud triangle explains the reason why someone performs a fraud. However, what exactly is fraud?

Fraud refers to a deceptive act caused by an employee or any member of the organization for personal gain. It can be intentional. It is an act to gain profit from illegal activity. Illegal acts can harm of parties involved.

For instance, An employee who commits fraud is earning extra profit than a promised salary or expense.

| ”Fraud is the daughter of greed.” ~ Jonathan Gash |

What Is The Fraud Triangle Theory?

Fraud Triangle theory was proposed in 1953. It was published in a paper named Other People’s Money. It is a social psychology of Embezzlement by a criminologist Dr. Donald Cressey.

He interviewed 133 convinced embezzlers in prison. He found people who committed white-collar crimes had few facts

- Most of the people did not grow up around the people who committed crimes for instance in a “bad neighborhood” or “criminal families”.

- They found “pressure” they couldn’t share.

- They saw “Opportunities” to escape from problems.

- They found a way to justify their actions.

This was a theory that provided the base for why people commit fraud.

3- Who Commits Fraud?

A stereotypical fraud looks like the result of a trusted employee. According to a report by the Association of Certified Fraud Examiners, 84% of employees who commit fraud had no criminal history. The majority of people committed this crime for the first time.

The people who commit fraud are their circumstances not a personality trait. Most people do this because of the particular circumstances.

The 10-8–10 rule states that 10% of people would never commit fraud for any reason, while 10% of the people are always looking for an opportunity to commit fraud. The 80% of them fall in between the both.

The people who fall in between are not like they aren’t fraudsters by nature or will not commit fraud throughout their lives.

For instance, An employee who never did any fraudulent activity within 10 years and suddenly he does a fraud because of the circumstances.

Every individual has a different set of circumstances. It has different combinations of fraud triangle components (motivation, rationalization, and opportunity). It makes fraud feel “worth it.”

Going deeper into the fraud triangle conditions, business owners can work to prevent them from affecting their employees.

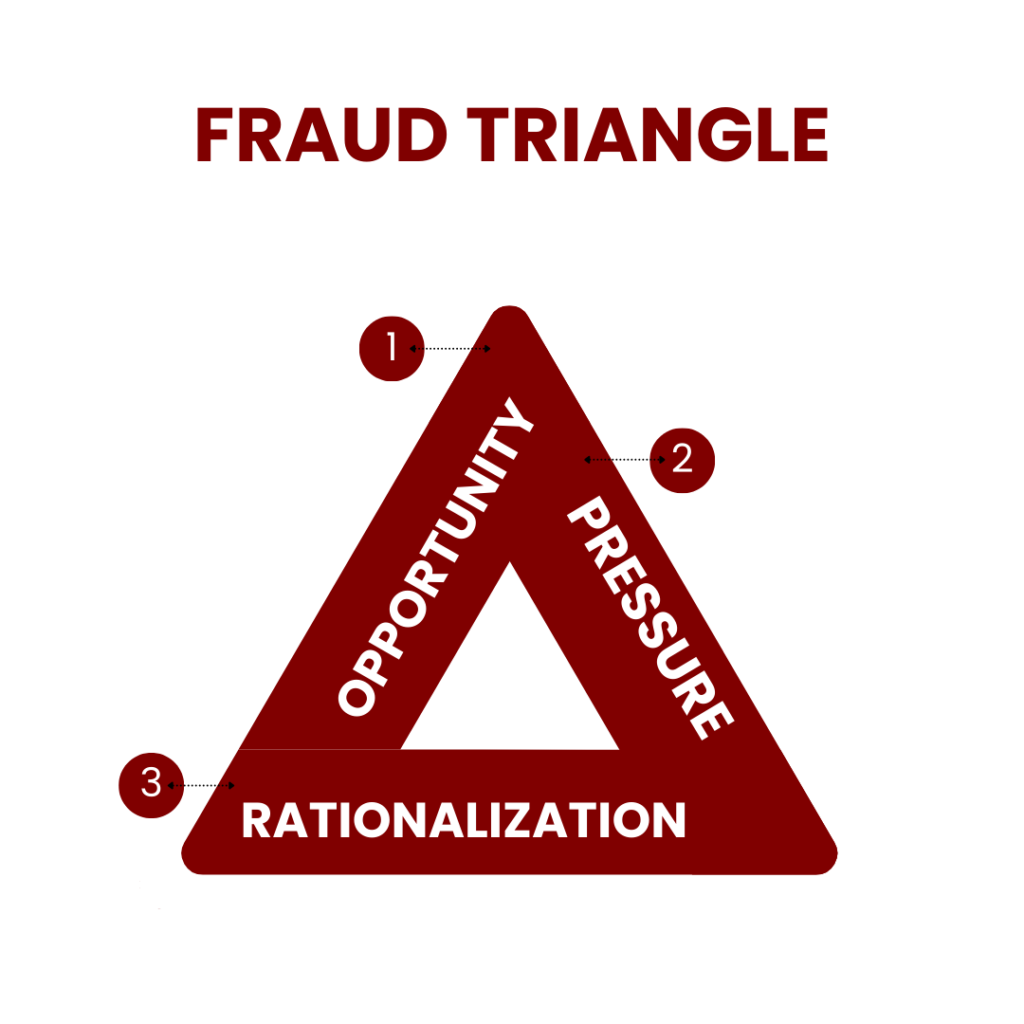

4- What Are The Three Sides Of The Fraud Triangle Theory

The fraud triangle is widely used by anti-fraud professionals these days. It explains the conditions under which employees can commit fraud. Companies are engaging in this model to prevent fraud.

This model can highlight the industry-specific conditions that can lead to risk. To identify risks and fraudulent activities, anti-fraud professionals look for these three sides of the fraud triangle theory.

Pressure, Motivation & Incentive:

The first and most important element of the fraud triangle is the incentive, motivation, or pressure to commit the crime.

What motivates a person to commit fraud? The person is looking for ways to solve their financial problems. It can come from personal problems or outside influences.

| “Pressure is what cracks pipes, not the fluids within them.” ~ Robert Tew |

Examples of financial issues or personal problems that can motivate one to commit fraud include

- Debts or high tax payments

- Inability to pay bills

- Addiction to drugs or alcohol

- perceived status and wealth

The ability to understand the employee’s potential motivation to commit fraud is based on how well you know them and their circumstances.

Spending time and noticing a strange activity and behavior as well as work can be a signal. Developing an understanding and one-to-one meetings with employees is the least help you can do.

How To Prevent Motivation-Based Fraud

You can take preventive measures to prevent motivation-based fraude. It can include

- You can support an empathetic environment to let them know that the company cares about their employee

- Let your staff know that you can provide help and assistance on hard days.

- Establish open communication channels to discuss any problem your employees face.

- Conduct regular check-ins to know their behavioral or personal issues.

- Recognize awards and ethical support to regard their work.

Opportunity

The second element of the fraud triangle is opportunity, also known as perceived opportunity.

At this stage, an individual identifies ways to commit fraud with the lowest calculated amount of risk. The person is willing to perceive that they can commit fraud without getting caught.

| “Opportunity makes a thief.” ~Francis Bacon |

A few examples of fraud opportunities include

- Lying about the number of work hours

- Lying about higher sales

- High productivity reports to receive higher pay

- Creating false invoices for products the company never purchased

- Selling the company’s information to competitors

Maintaining social status is the common motivation for committing fraud. Lack of supervision of employees can cause opportunity-based fraud. Inadequate internal controls audit can lead to fraud.

How To Prevent Opportunity-Based Fraud

To prevent opportunity-based fraud, the company should implement several key controls, which include

- Segregate the responsibilities for adding new vendors, processing invoices, and authorizing payments.

- Conduct periodic audits of internal systems and payment transactions

- Thorough background checks and validation of their business credentials.

Rationalization:

The third Element Of The Fraud Triangle Is Rationalization.

After identifying the motivating factors and opportunities to commit fraud, fraudsters rationalize that they are doing the right thing.

Fraudsters convince themselves that theirs is a victimless crime. Offenders don’t see themselves as criminals. Regular people are caught in a bad situation.

Examples of rationalizations include

- “Borrowing” of money

- Perceived low pay

- Worked long hours with no additional compensation

- Didn’t feel respected or appreciated

- Just trying to pay the bills

How to prevent Rationalization-based fraud:

To prevent rationalization-based fraud, the company can take preventive measures which can include

- Implementation of ethical training programs to boost the employee’s morale.

- Promote a culture of transparency and accountability.

- Identify the common rationalization concerns and processes

- Encourage fair treatment with all employees.

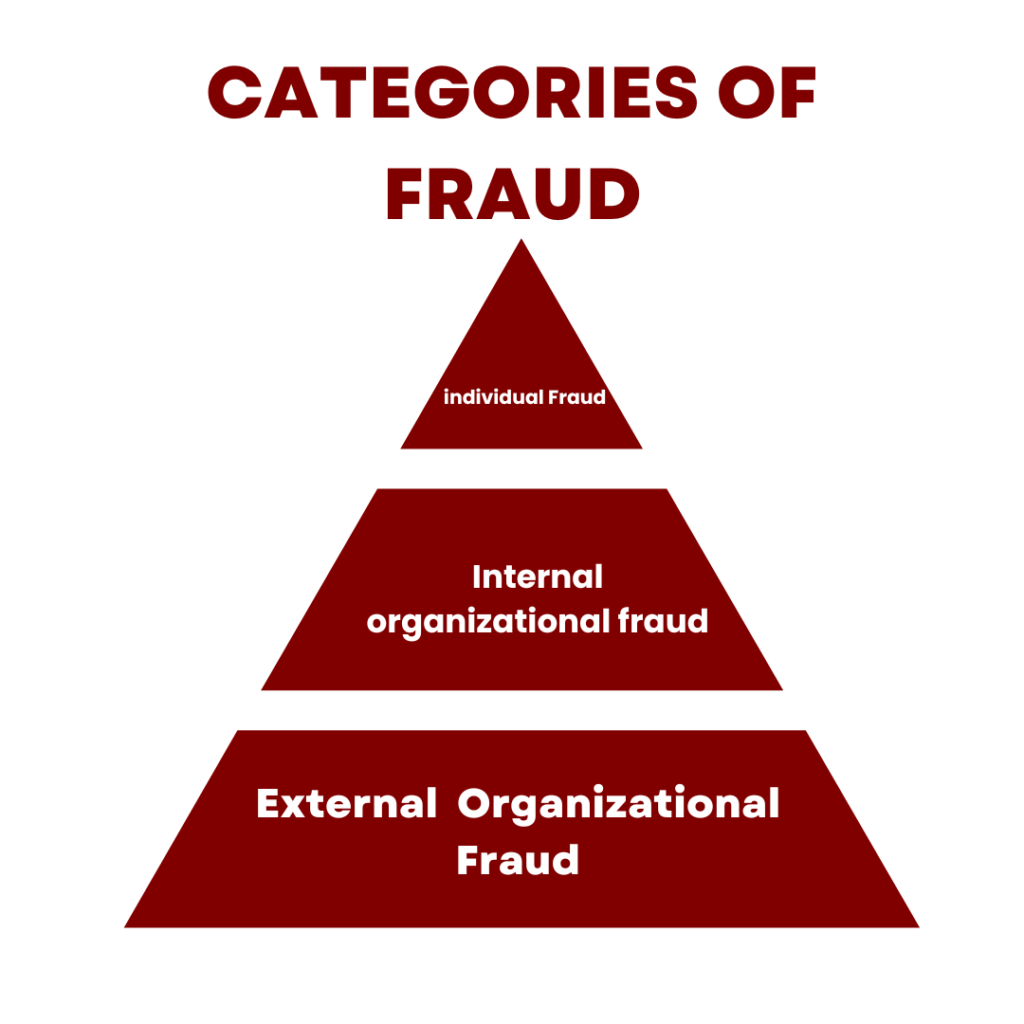

5- Categories Of Fraud

Fraud is so common and it can be categorized in countless ways. But fundamentally, every type of fraud can be organizational or individual. The key characteristics of each type can be

Against Individuals:

When a single person is targeted and involved by a fraudster it falls in against an individual fraud. It can include identity theft and advance fee schemes. The most common and devastating individual fraud includes The Ponzi scheme.

Internal Organizational Fraud:

When someone in an occupational fraud deceives a group of people for instance it can involve an employee, manager, or any executive of the company to deceive the company. Cheating on taxes and lying to investors and shareholders fall in this category.

External Organizational Fraud:

This fraud is committed in an organization from the outside. People outside the company such as vendors involved, in bribes demanded from employees, can involve in external organizational fraud.

Suggested Read: Regulatory Compliance: Definition, Examples, Insights, And More

6-How To Protect Your Company Under Fraud Triangle

The risk to lower fraud can be minimized if the triangle of fraud elements are lower. Organizations and companies should make the possible solutions to cater all the elements for minimizing the fraud risk. Organizations can take a few steps which can include

Reduce Pressure On Your Employees

Companies should set realistic and achievable targets to reduce the risk of accounting fraud.

New employees should be informed of previous fraudulent behavior. Pressure and poor treatment by a company can put a person at risk as well as finances. If employees feel they can talk about financial or personal issues it should be promoted.

Reduce Opportunity With Internal Controls And Software

Internal control measures should be implemented to record the employee’s activities. Duties should be segregated for checks and balances of employees’ performance.

The right software can help in preventing, monitoring, and detecting occupational fraud.

Reduce The Opportunities For Rationalization

Company culture should be open, transparent, and ethical. A clear fraud detection plan should be in process to detect and prevent rationalization.

All employees should receive regular training on avoiding and detecting fraud also they should be able to report it freely.

Final Thoughts

The fraud triangle reveals insights into a person’s behaviors based on the framework and theory Recognizing red flags and working on them to prevent fraudulent activities is very crucial for companies. Prevention is better than cure. A perfect storm of psychological and environmental factors is exposed with this model. The understanding and implementation of all interconnected measures can minimize the fraud risk triangle.

FAQs

What Are The Stages Of The Fraud Triangle?

There are three stages of the fraud triangle which include

- Pressure

- Opportunity

- Rationalization

What Is The New Fraud Triangle?

The new fraud triangle model is a new version of Cressey’s original theory by integrating motivation, opportunity, integrity, and fraudster’s capabilities.

What Is An Example Of Fraud Triangle Rationalization?

Examples of Fraud triangle rationalization are “I am not stealing the money” or “I work for a company and I owe the money I am stealing”.

What Are The Three Critical Types Of Fraud?

Critical types of fraud include

- Fraud Against individuals

- Internal organizational fraud

- External organizational fraud

What Is The Fraud Triangle?

The Fraud Triangle is a criminological framework of why individuals commit fraud by identifying three key factors pressure (motivation), opportunity, and rationalization

Which Of The Following Is Not A component Of The Fraud Triangle?

The element that is not part of the Fraud Triangle is “trust.”

+ There are no comments

Add yours