In this developed era, Digital threats loom large in the financial sector. the European Union introduced the Digital Operational Resilience Act (DORA) as a game-changing regulation. It takes effect on January 17, 2025.

This act is poised to enhance the cybersecurity threats for financial institutions around the EU. Cybersecurity attacks in Poland banks on average happen 1,600 per day. This score underlines digital resilience more critically.

DORA’s impact is beyond traditional financial entities. It extends to ICT service providers. The interest in staying non-compliance is high.

The fines for non-compliance are up to 2% of the global annual loop or €10 million that’s higher. The personal liability introduced by DORA for C-suite executives reached penalties of up to €1 million. It highlights the urgency to mitigate compliance

The financial institutions face the race against time when the deadline approaches. According to a recent report, 43% of the financial services companies in the UK anticipate missing the Dora compliance deadline by the last three months.

With the growing rate of Cyber threats, and technological disruptions regulatory demands are increasing. It is essential for organizations to adhare to these frameworks to prevent their operations.

The Digital Operational Resilience Act (DORA) is a regulation designed for the financial sector’s ability to stand and overcome ICT-related disruptions. This blog post will help you explore how financial institutions can achieve Dora Digital Operational Resilience Act Compliance with actionable insights.

What Is The Digital Operational Resilience Act?

The Digital Operational Resilience Act, commonly referred to as DORA is an EU regulation that establishes a comprehensive regulatory framework and ensures financial entities maintain operational resilience against ICT (Information and Communication Technology) risks.

It was proposed by the European Commission in September 2020 and set to take effect on January 17, 2025.

This regulation applies to a range of financial entities. It includes banks, insurance companies, investment firms, payment institutions, and other financial entities operating in the EU.

It also includes third-party ICT service providers. The main aim of the act is to strengthen the cybersecurity and operational resilience of the financial institutions. It creates a unified regulatory framework for digital operations.

It is a pivotal piece of legislation that ensures the financial sector can prevent, respond, and recover from ICT-related incidents.

Adhering to this act financial institutions can continue to operate without the fear of being stuck in cyberattacks. It highlights the importance of digital operational resilience.

The Objectives Of The Dora Act

The Digital Operational Resilience Act (DORA) has multiple objectives including

Improved ICT Risk Management

Financial groups and institutions must implement ICT risk management processes to identify, analyze, assess, and mitigate ICT-related risks.

Upgraded Incident Reporting

Organizations should propose clear and transparent procedures for reporting major ICT-related incidents and events to regulatory bodies.

Enhanced Third-Party Risk Management

The Digital Operational Resilience Act Dora requires that financial institutions assess and monitor the risk related to their ICT third-party service providers.

Encouraged Operational Resilience Testing

Regular testing of ICT systems and processes ensures the Standardize operational resilience. It is the core requirement across the EU financial sector.

Assuring Information Sharing

The regulation assures financial institutions to share information about cyber threats to enhance joint resilience

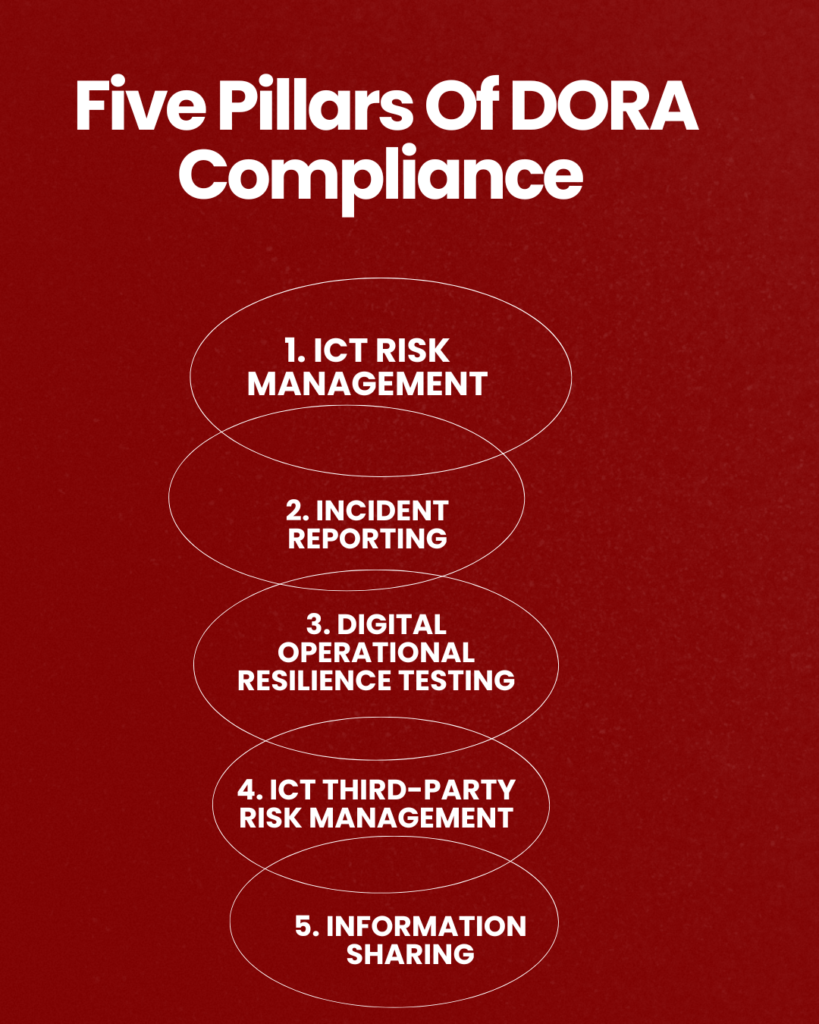

The Five Pillars Of DORA Compliance

Digital Operational Resilience Act has five pillars that every financial institution should follow to achieve compliance with the DORA Act. The five pillars include

1. ICT Risk Management

Financial entities are encouraged to implement in-depth ICT risk management strategies and frameworks including

- Classification and documentation of all ICT-related risks

- Applying preventive measures for protecting the risks

- Analyzing anomalies and incidents

- Devise complete response and recovery procedures

- Learning from continuously evolving methodologies

2. Incident Reporting

DORA mandates a standardized process for reporting significant ICT-related incidents. Key aspects include:

A standardized process is necessary for ICT-related incidents under DORA. The different aspects of reporting include

- Integration of events based on their severity and impact

- Adhering to time timelines

- Report the initial notification within 24 hours

- Report the incident within 72 hours

- Document the final report within one month

| A piece of detailed information about the incident its nature and its impact can help in advising mitigation measures about the event. |

3. Digital Operational Resilience Testing

Continuous and regular testing of digital operational resilience is one of the core components of DORA. it includes

- Overseeing the annual threat-led penetration testing (TLPT). It usually conducted on high-value assets

- Assuming real-world cyberattacks to identify sensitivities.

- Testing technical controls replies in incident response

- Organizational processes help in response to capabilities.

4. Ict Third-Party Risk Management

DORA emphasizes the importance of managing risks associated with third-party ICT service providers. Financial institutions must:

DORA Act highlights the importance of risk management that is related to third-party ICT service providers. Financial sector must

- Analyze and monitor the risks from third-party providers

- Implement and advise contractual arrangements

- Ensure the resilience standards with third-party providers as the financial institution itself

5. Information Sharing

DORA Act encourages information sharing about cyber threats to enhance the overall resilience in the financial sector

DORA Act Timeline

Digital Operational Resilience Act timeline is important to understand to ensure compliance on time. The milestones of the act include

| Milestone | Timeline |

| Proposal by the European Commission | September 2020 |

| Adoption by EU Parliament | Expected in 2023 |

| Entry into Force | Expected in 2025 |

| Compliance Deadline | 12-24 months after entry into force |

Dora Act Compliance: A Step-By-Step Process

A systematic approach is required to achieve compliance with the Digital Operational Resilience Act (DORA). A detailed step-by-step process financial institutions can follow includes

1. Governance And Leadership

A digital Digital Resilience Officer or team can help in achieving compliance on time. Appoint A digital Digital Resilience Officer to conduct direct reporting from senior leadership

- A compliance committee with members can ensure the oversight of various departments

- Integrate digital resilience for overall business strategy and risk management processes

2. An In-Depth Gap Analysis

Analyze and evaluate ICT-related risk with existing procedures and governance procedures against the requirements of DORA.

- Recognize all the procedures and methods that will be affected by DORA.

- Decide if your organization is capable of any exemptions from specific DORA requirements

3. Deep-Dive Asset Mapping

Use advanced tools that can automate and configure the management databases (CMDBs) to scan the catalogs of IT assets.

- Map out the interdependencies of the IT ecosystem

- Configure the on-premise hardware software, cloud services, and third-party dependencies

4. A Thorough Risk Assessment

Risk assessment tools help to identify the risks. Employ these tools within your digital systems to identify these risks.

- Invest in automated vulnerability assessments, intelligence tools for threat analysis, and penetration testing to reveal the critical gaps in a specific area.

- Develop an approach to test the risk intensity. It can include physical testing, application testing, and technology resilience testing.

5. Ict Risk Management Framework

An in-depth and comprehensive ICT risk management procedure can help to mitigate the risks. Implement this approach to protect your organization from overall risk.

- Set risk identification processes, risk detection, response, and recovery.

- Assure regular assessments to adapt to the evolving threats.

6. Incident Management And Reporting

Advise procedures to detect and manage ICT-related incidents and reporting.

- Execute a classification system for incident management

7. Information Sharing Arrangements

Take part in cyber threat information and information sharing sources with other financial entities.

- Provide notification to authorities for information-sharing arrangements

8. Monitoring And Improvement Continuously

Monitor your DORA’s developments with regulatory updates continuously.

- Stay in relationship with regulatory bodies and experts for updates

- Prepare and adapt your organization to changing regulations to stay compliant

DORA vs. Existing Regulations

To understand the impact of the Digital Operational Resilience Act EU. let’s see how it differs from existing regulations

| Scope | DORA Act | GDPR |

| Focus | It is ICT and operational resilience in finance | It protects data and privacy |

| Scope EU | It applies to financial entities and ICT providers | It applies to All organizations processing EU residents’ data |

| Incident Reporting | It has strict timelines | Reporting incidents within 72-hour notification for data breaches |

| Testing Requirements | It includes annual threat-led penetration testing | It presents Data protection impact assessments |

| Penalties | It can cause penalties Up to 1% of daily worldwide turnover | It can cause penalties Up to 4% of annual global turnover |

Challenges In Achieving Dora Act Compliance

Financial institutions can face several challenges in achieving DORA Act compliance including

Complex Implementation

The nature of DORA requirements poses a complex implementation process. Financial institutions must pursue their existing ICT risk management frameworks.

This often includes the changes to establish processes and systems.

Allocation of Resources

DORA compliance demands significant human resources as well as financial.

The institutions struggle to allocate the necessary resources with a limited budget with requires changes, especially with strict timelines for compliance.

Third-Party Risk Management

Including third parties for DORA compliance poses a challenge. Financial institutions need to assess and monitor the risks associated with ICT service providers.

It becomes extremely complex for organizations with extensive networks.

Continuous Testing and Improvement

Regular digital operational resilience testing requires threat-led penetration testing and it poses challenges for ongoing processes.

Financial institutions must develop testing frameworks to address and update the evolving cyber threats.

Incident Reporting Timelines

DORA’s strict incident reporting timelines sometimes become complex. Initial notification within 24 hours and intermediate updates within 72 hours are complex to meet.

For some incidents, it’s mandatory and complex as well.

Regulatory Alignment

Regulatory requirements are evolving in nature and aligning with them adds an extra layer.

For instance, GDPR and NIS2 are regulations that are complicated to meet. Institutions must ensure compliance with multiple regulatory frameworks.

Technological Gaps

Financial institutions face technological gaps with existing ICT infrastructure.

Updating systems to meet DORA’s requirements for resilience and security is a costly and time-consuming process.

Cultural Shift

cultural shift for prioritizing digital operational resilience across all levels of the organization is important to implement.

It changes the thinking toward challenges, especially with institutions with rooted practices

Keeping Pace with Evolving Threats

The increasing cyber threats highlight that compliance is not a one-time effort. It requires continuous adaption to changing strategies.

To stay ahead of the curve of these challenges institutions need to adopt new advancements.

Final Thoughts

The EU Digital Operational Resilience Act (DORA) represents a game-changing approach. It strengthens the EU financial sector’s ability to recover from ICT-associated disruptions. It provides stricter cybersecurity and operational resilience measures.

By focusing its pillars on ICT risk management, testing against resilience, third-party risk management, and information sharing financial institutions can achieve and comply with overall operational resilience.

Financial institutions must follow the deadlines before approaching to avoid penalties to prevent digital infrastructures.

FAQs

What is the Digital Operational Resilience Act?

The Digital Operational Resilience Act, commonly referred to as DORA is an EU regulation that establishes a comprehensive regulatory framework and ensures financial entities maintain operational resilience against ICT (Information and Communication Technology) risks.

It was proposed by the European Commission in September 2020 and set to take effect on January 17, 2025.

This regulation applies to a range of financial entities. It includes banks, insurance companies, investment firms, payment institutions, and other financial entities operating in the EU.

What are the 5 pillars of DORA?

The five pillars of the Digital Operational Resilience Act summary include

1. ICT Risk Management

2. Incident Reporting

3. Digital Operational Resilience Testing

4. Ict Third-Party Risk Management

5. Information Sharing

What are the principles of the Digital Operational Resilience Act?

The five principles of the Digital Operational Resilience Act (DORA) include

- ICT risk management,

- Incident reporting

- Digital operational resilience testing

- ICT third-party risk management

- Information Sharing

Who needs to comply with DORA?

Financial institutions of a wide range of need to comply with DORA including

- financial entities

- ICT third-party service providers operating in the EU

- Banks

- Insurance companies

- Investment firms, and payment institutions

You may like to read:

+ There are no comments

Add yours